The Longevity Biotech Funding Landscape

As aging comes to be seen as a malleable process rather than an inevitable fate, the longevity biotech sector is drawing billions in investment. In this post, we dive into the current state of the longevity biotech funding landscape, analyzing fundraising trends and the emerging ecosystem of startups that are working to redefine human health and lifespan. Drawing from data collected through Longevity List and Pitchbook, this report provides a snapshot of where the industry stands today.

We define longevity biotech companies based on the Longevity Biotech Landscape. Focusing solely on therapeutics, we’ve excluded cryonics, diagnostics, supplements, nutraceuticals, and topical cosmetics to zero in on companies that:

- Target the biological mechanisms of aging or address pathological manifestations underlying age-related diseases that affect multiple organs or systems, or

- Focus on regenerative medicine, aiming to restore or maintain health and vitality as people age.

With the longevity biotech sector at a turning point, this report aims to offer a health check on the market, providing key insights into the companies and investors driving the future of human health and lifespan.

2024 Funding Overview

1. Longevity biotech is in recovery after a brutal 2023

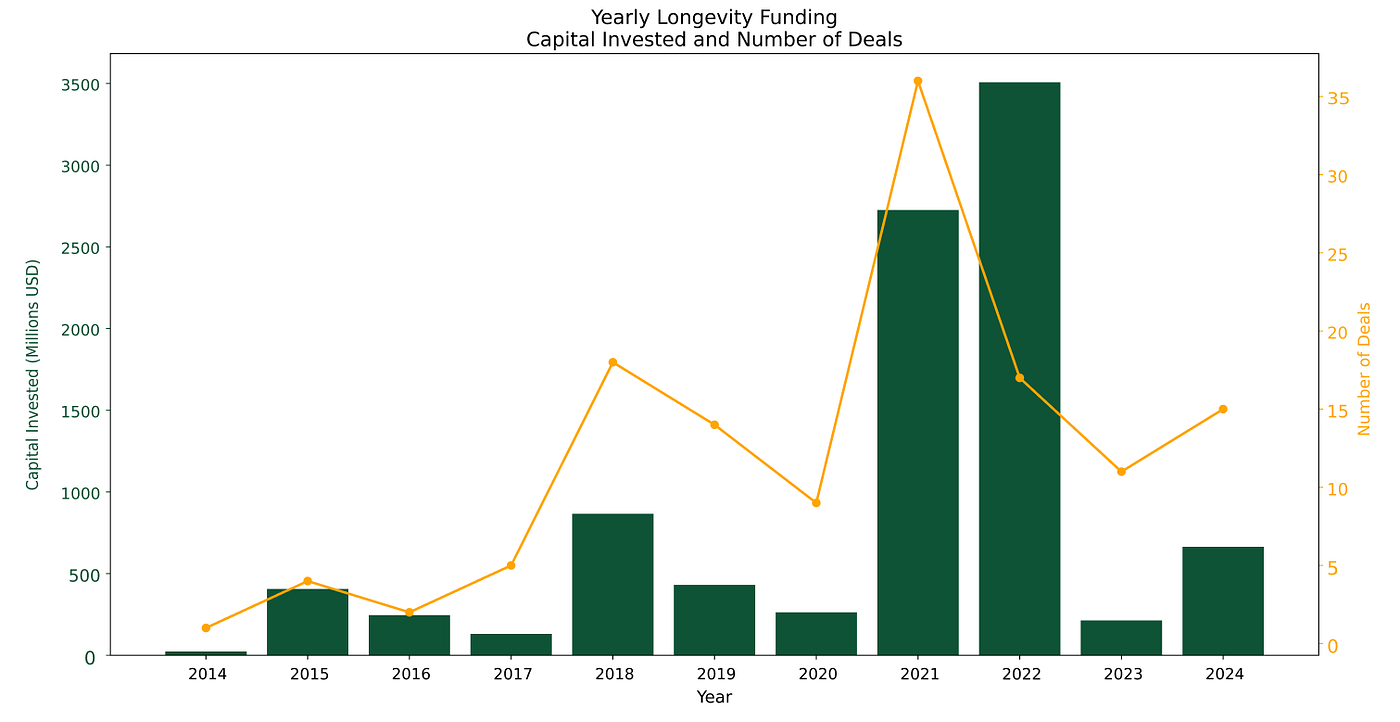

Similar to many other industries, such as deeptech and software, the longevity biotech sector faced a tough market in 2023, experiencing its lowest funding levels in five years. However, 2024 has seen a notable recovery, with total financing reaching $664.4 million so far, a significant increase from the $213.4 million raised in 2023. The number of deals has risen to 15, up from 11 in the previous year. With 2024 still underway, the yearly total will even be higher.

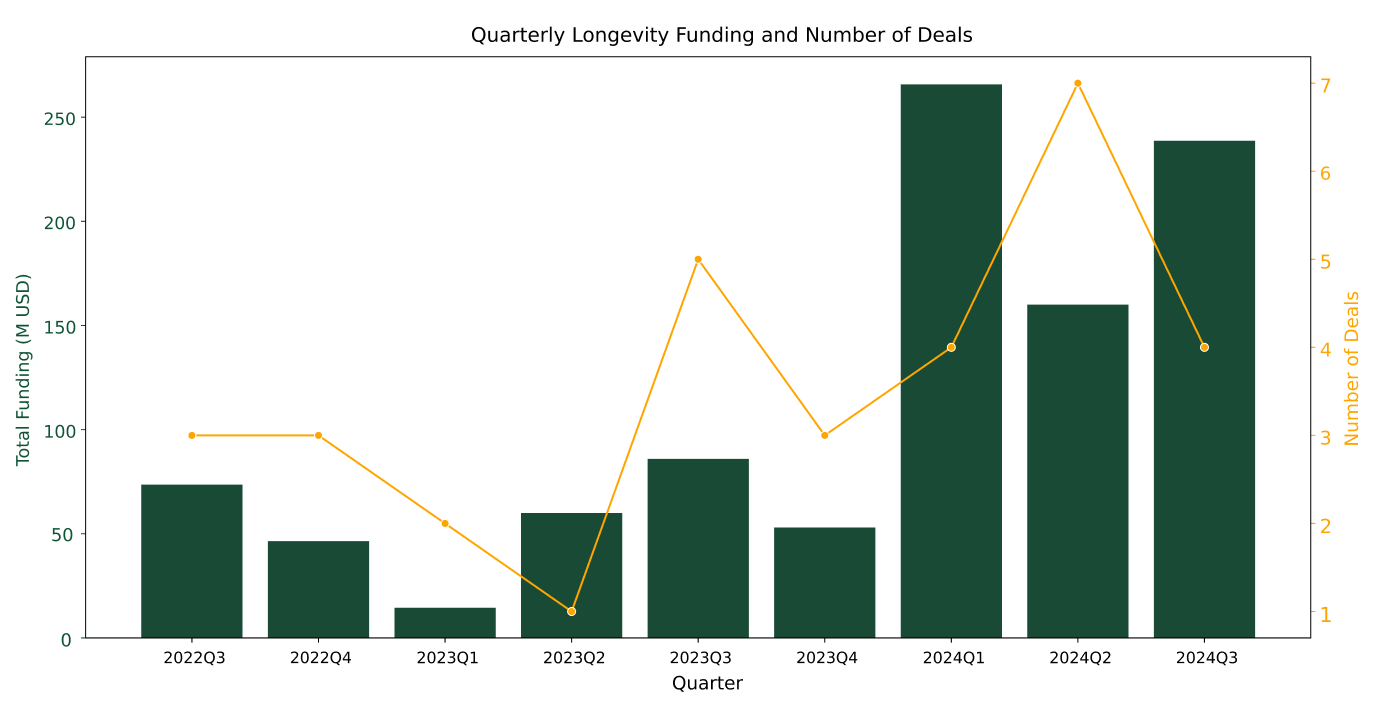

The financial landscape in Q1 2024 started off strong, with $265.72 million in total funding — surpassing the entire yearly funding for 2023. This suggests the sector’s recovery began early in the year.

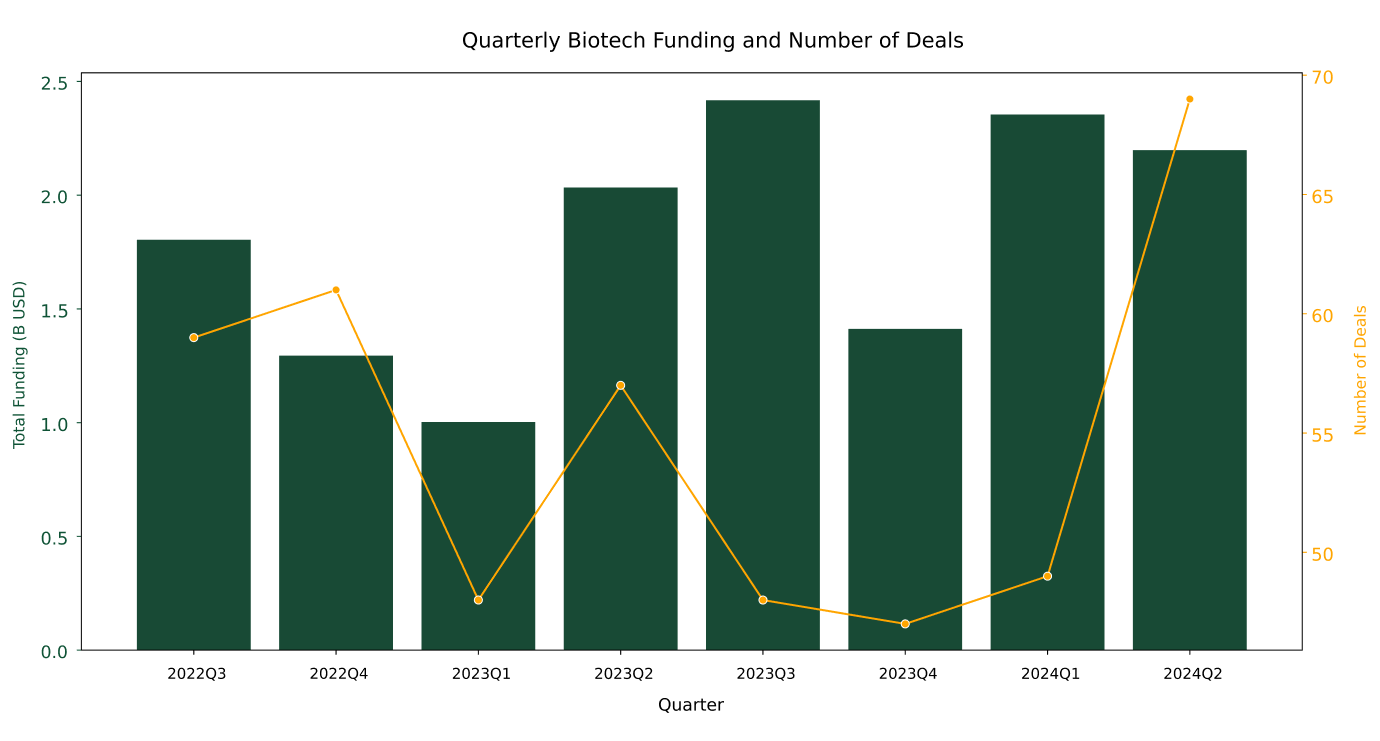

Compared to broader biotech, longevity biotech has shown far more volatility. In Q1 2024, funding in the sector surged 10x compared to the same period in 2023, easily surpassing broader biotech’s more modest 2x growth.

This reflects the speculative nature of the field. While traditional biotech’s recovery has been more linear, driven by steady pipeline progress, longevity remains event-driven and reactive. The potential rewards are higher, but so are the risks. Investors are holding back, waiting for clear breakthroughs before committing to consistent capital flows.

2. Recovery favors scaling companies: mega rounds are reserved for established players while new ventures stagnate

The 2024 funding landscape signals maturity. Series A and later rounds now dominate, capturing 42.9% of total funding, up from 27.3% in 2023, as investors focus on scaling established companies. The emphasis is clearly on backing proven ventures, rather than nurturing new startups.

This shift mirrors broader biotech trends, where rising interest rates and constrained liquidity have led to a flight to quality. New venture formation has stalled, with first seed rounds remaining low in both 2023 and 2024.

Unlike the 2021–2022 boom, where we witnessed seed-stage mega rounds, particularly for partial reprogramming ones like Altos Labs’ $3B and Retro Biosciences’ $180M, 2024 has seen a notable contraction in seed-stage funding. Today, the $100M+ club is reserved exclusively for Series D rounds, and only two companies, BioAge and eGenesis, have crossed that threshold. Still, it’s a step forward from 2023, where no deals of this scale were reported, underscoring a gradual recovery in the ecosystem’s upper tiers.

For established players, this tighter market is an opportunity. Existing companies with strong foundations are well-positioned, while fewer new startups reduce competition. However, the slowdown in new ventures risks limiting future breakthroughs. 2024 is shaping up as a year of consolidation, with the recovery concentrated in later-stage companies, leaving new company formation flat.

3. Longevity biotech has its first IPO since 2021; obesity is the new longevity indication

Keeping up with the theme of recovery for later-stage companies, BioAge raised $198 million in its IPO on September 26th, marking the first public offering in the longevity biotech sector since 2021. Starting out as a drug discovery platform, the company has shifted to the obesity market through its partnership with Eli Lilly to develop azelaprag, a drug aimed at preserving muscle mass in combination with GLP-1 agonists.

BioAge’s move into the weight-loss drug market — one of the hottest areas in biotech — reflects a larger shift in obesity being viewed as a key longevity indication. Obesity, much like aging, is a risk factor for many diseases rather than a disease itself. With metabolic pathways like AMPK and mTOR being well-validated in longevity science, the pivot to treating obesity through these pathways aligns with the goal of extending healthspan. This trend is echoed by other longevity biotech companies, such as Oisin Bio’s recent series A to develop therapies to eliminate fat cells and Fauna Bio’s research in partnership with Lilly to discover new obesity targets.

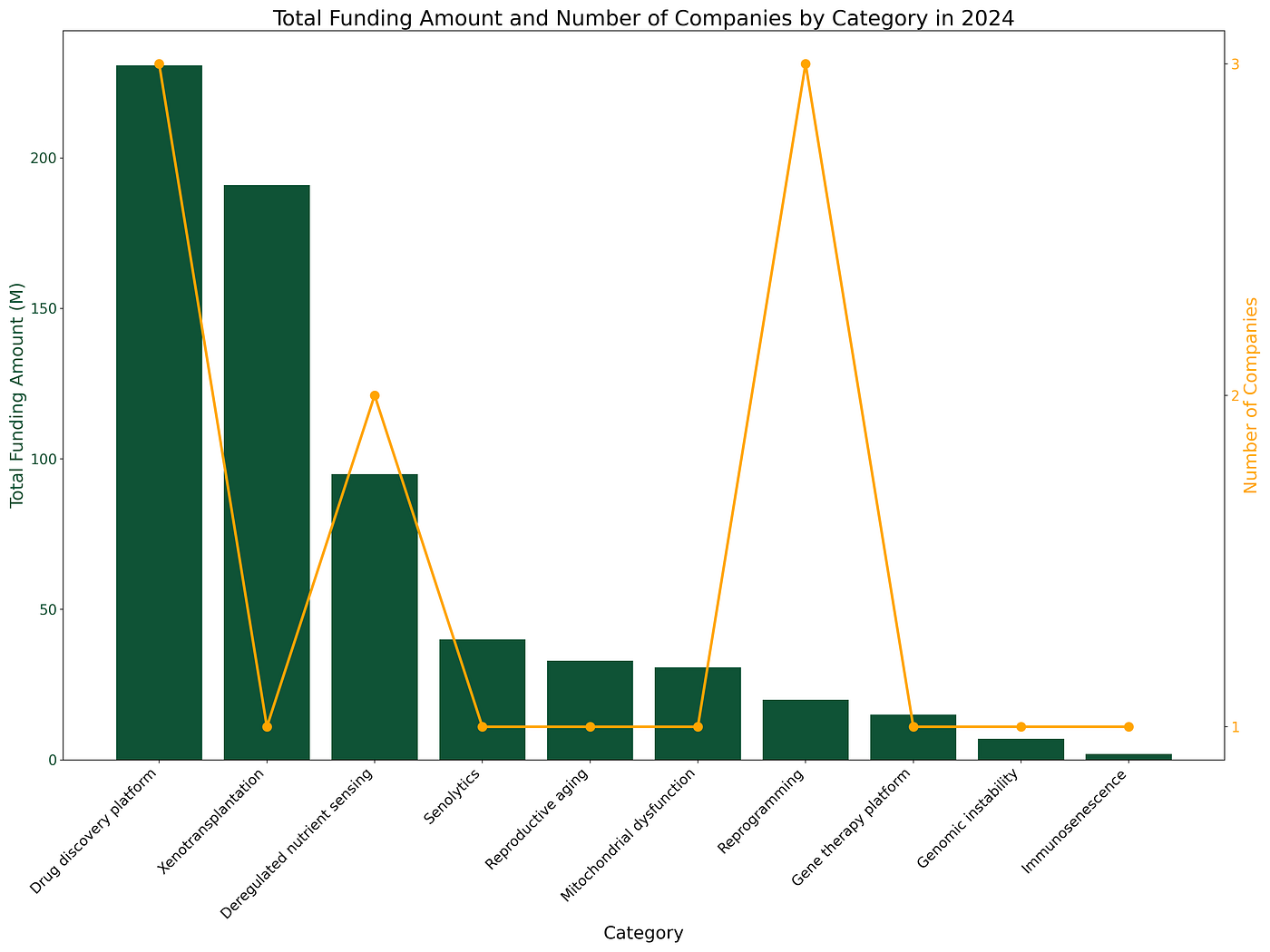

4. Drug discovery platforms dominate the funding landscape; reprogramming hype still present

Drug discovery platforms make up the most number of deals and also the number of amounts raised in 2024. This focus on platform technologies highlights investors’ appetite for new longevity targets and mechanisms to pursue. This highlights a key trend: investors want exposure to multiple shots on goal, looking for mechanisms that can be deployed across diverse therapeutic applications, rather than backing more singular, high-risk bets.

Partial reprogramming, on the other hand, tells a more nuanced story. While it raised only $20M this year — a significant drop from its blockbuster year in 2022 — it still boasts the highest number of active companies. This suggests that while investors may be taking a more cautious approach in terms of capital deployment, the innovation ecosystem remains bullish on reprogramming’s potential. The surge of companies focused here points to ongoing belief in its eventual breakthroughs, despite the current dip in financial enthusiasm.

What we’re seeing is a bifurcation in the market. On one side, there’s a growing preference for platform technologies with nearer-term commercial prospects, especially those that are closer to the clinic or offer clearer paths to market. On the other, you have areas like reprogramming, where investor sentiment has cooled somewhat, but where the number of innovators continues to grow. This dynamic reflects a maturing sector, where proven approaches get the bulk of the capital, but bold, paradigm-shifting technologies still draw significant entrepreneurial attention. It’s a reminder that even as some areas temporarily fall out of favor with investors, they often remain fertile ground for innovation.

Overall Funding Landscape

1. Longevity biotech is a growing but still nascent industry

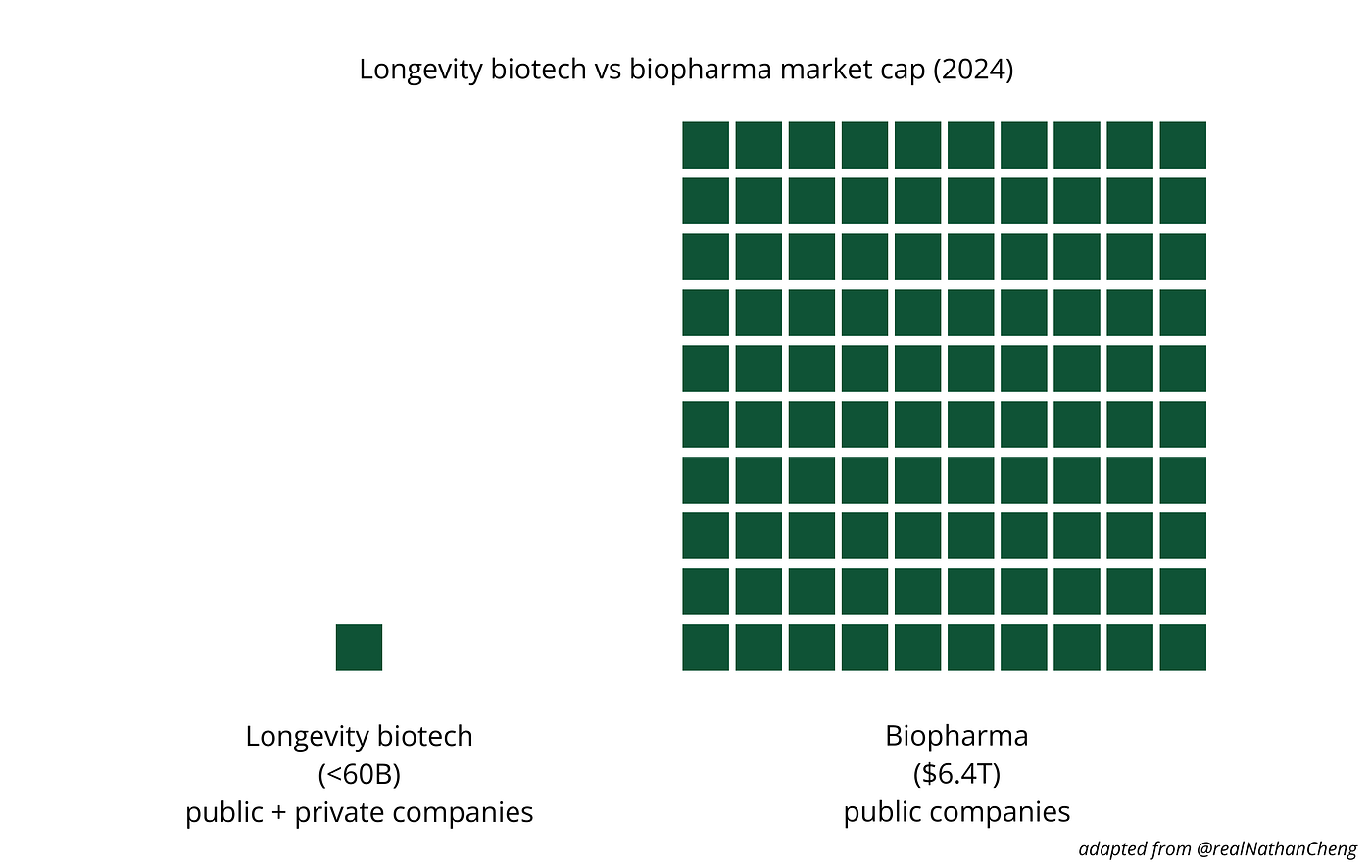

Over the past decade, longevity funding has surged by 30x, climbing from $23.5M in 2014 to $664.42M in 2024, with a peak of $3.5B in 2021 — a remarkable 148x increase. However, when compared to broader biopharma, longevity biotech remains a niche sector, receiving just 2.9% of total biotech funding and representing less than 1% of the $6.4 trillion biopharma market cap. Despite rapid growth, this highlights how longevity biotech is still in its infancy, presenting significant untapped potential for both investors and innovation.

2. Not all categories are funded equally, revealing key areas with untapped potential

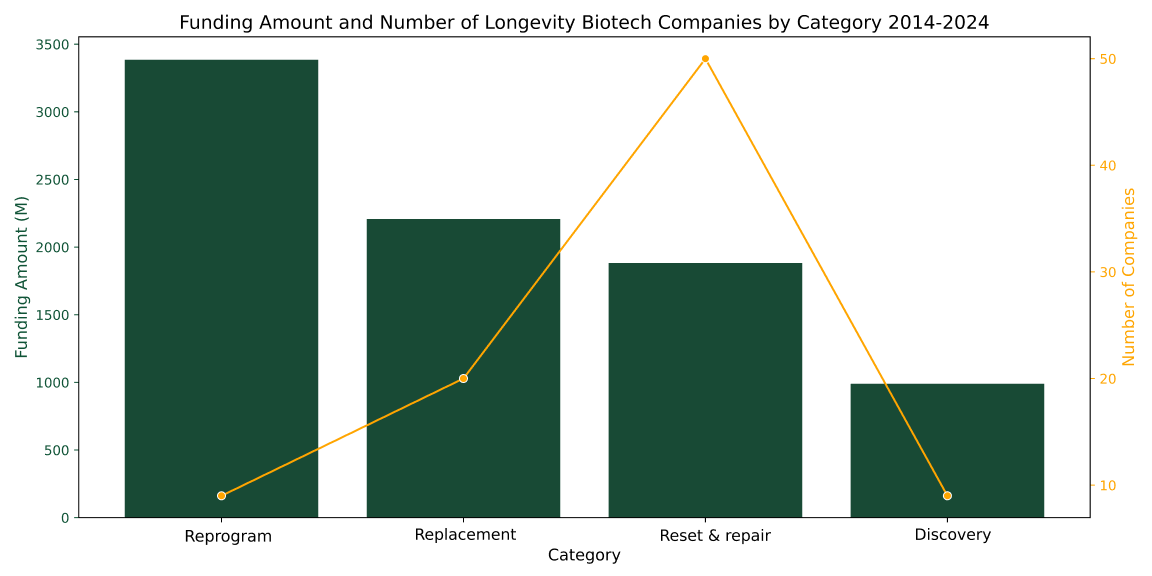

Based on the Longevity Biotech Landscape, companies in the sector can be broadly categorized into four paradigms:

- Reset and Repair: This paradigm focuses on targeting specific, known age-related pathways, factors, or damages identified in hallmarks of aging (2023) (with some modifications)

- Replace: Falling within the domain of regenerative medicine, this paradigm includes the replacement of aged cells, tissues, organs, or even the whole body with younger counterparts or endogenous regeneration.

- Reprogram: This paradigm is inspired by the natural rejuvenation process that occurs during early embryonic development, which enables the production of youthful offspring from old gametes. It aims to activate a similar embryonic-like program within aged cells, without altering their cell identity, through a process known as partial reprogramming.

- Discover: This paradigm focuses on identifying novel targets or interventions for aging by analyzing extensive datasets using advanced machine learning techniques. As companies here mature, they may eventually align with one or more categories in “Reset and Repair” or create a new category as their targets become more defined.

In the past decade, Reprogram companies have attracted the most funding, amassing a significant $3.5B, largely driven by heavyweights like Altos Labs. Interestingly, over this period, Discover is the least funded category, but in 2024, it received the highest amount of funding across the board, signaling a marked shift in investor attention. This shift reflects the growing maturity of Discovery companies, which are now demonstrating that their platforms can successfully identify drugs that progress into the clinical pipeline, as seen with companies like BioAge. Additionally, the rise of AI has played a pivotal role, with AI-driven drug discovery platforms capturing increased investor attention and reshaping the funding landscape.

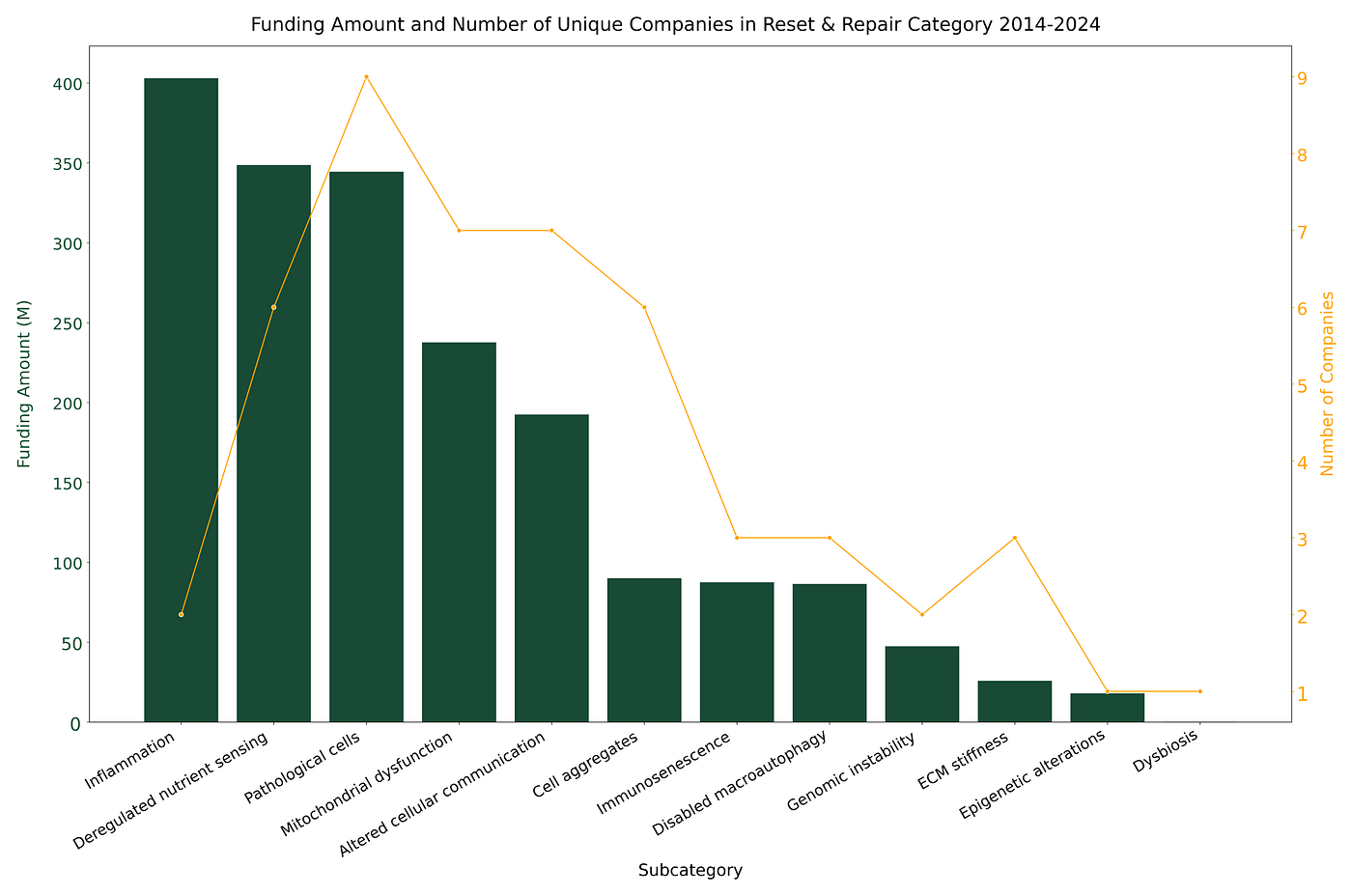

The Reset and Repair category has the largest number of companies, unsurprisingly, given the field’s traditional focus on addressing well-known, age-related pathways and damage. Within this category, deregulated nutrient sensing and pathological cells take the lead, both in terms of funding and the number of players. Metabolic pathways have long been among the most validated mechanisms in longevity research, and the surge of interest in targeting pathological cells, particularly senescent cells, has exploded after Baker et al. (2016) demonstrated that senescent cell removal increased mice median lifespan by more than 35%. Inflammation is another well-funded area within this category, though unlike the previous two, much of that funding is concentrated in a single company, Denali Therapeutics, which focuses on neuroinflammation.

On the other hand, the sub-categories within Reset and Repair with the least funding and fewest companies include genomic instability, extracellular matrix (ECM) stiffness, epigenetic alterations, and dysbiosis. While genomic instability and ECM stiffness are well-established contributors to aging, progress in these areas has been limited by the lack of tools to effectively target them. This creates a potential opportunity for innovation and investment. Epigenetic alterations and dysbiosis, on the other hand, are less defined — especially dysbiosis, which has only recently been recognized as a hallmark of aging.

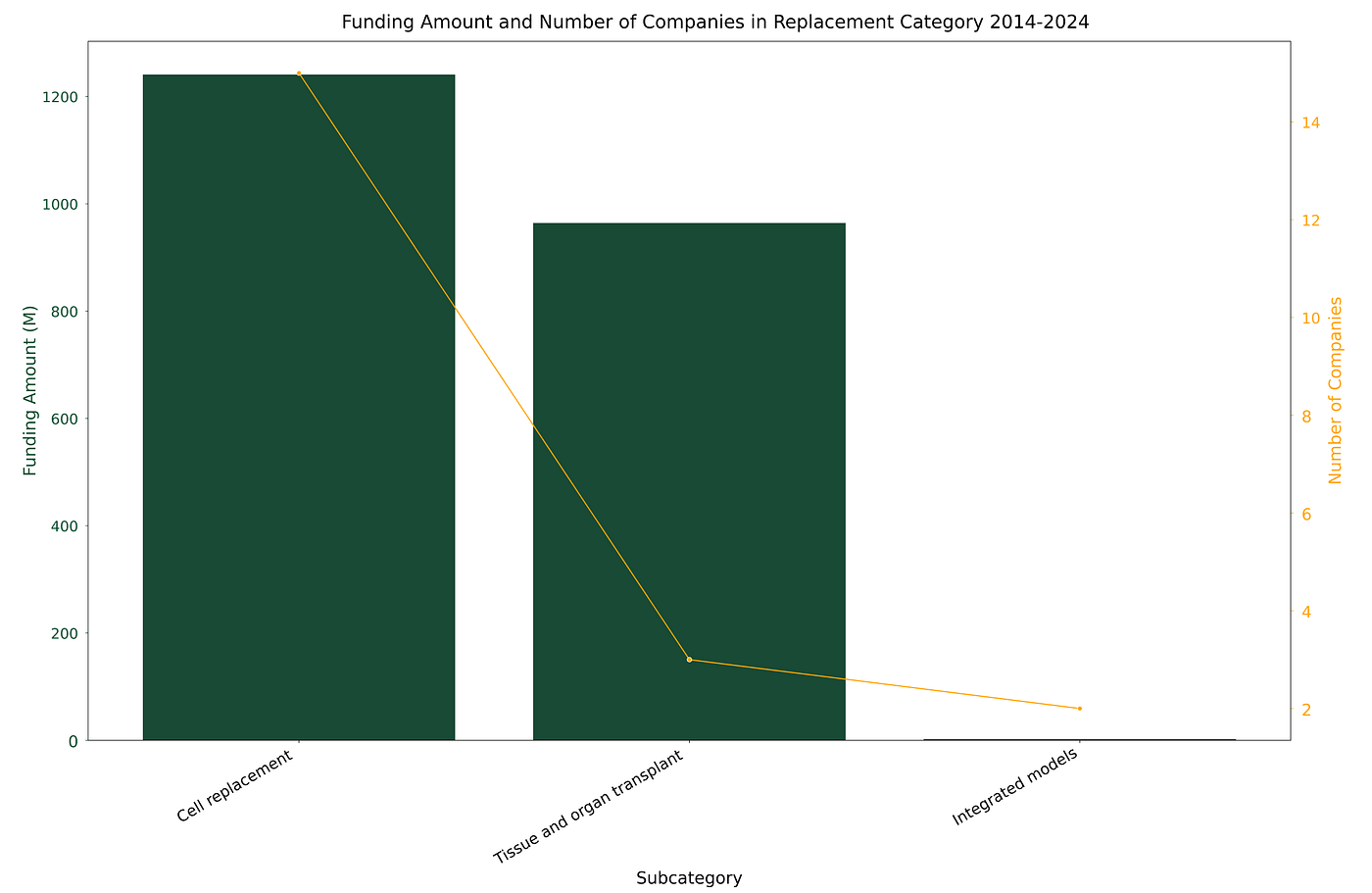

In the Replacement category, cell replacement continues to dominate, with over $1.2B in funding and the largest number of companies betting on stem cell therapies and regenerative medicine to combat aging. But tissue and organ transplants are quickly gaining ground. Despite fewer companies in this space, the subcategory has nearly matched cell replacement in funding, signaling concentrated bets on high-potential players. A prime example is eGenesis, which secured a notable $191M this year, underscoring growing confidence in xenotransplantation and advanced transplant technologies.

On the other hand, integrated models — focused on combining biological systems to replicate complex organ functions — remain niche, attracting limited capital and involvement from just a few companies. Interest in this area spiked after a 2021 breakthrough where researchers successfully cultured mouse embryos ex utero through critical developmental stages. While still early, integrated models are beginning to capture attention and could represent a frontier worth watching as the technology develops.

2. Founded year to funding time has decreased over time

The data clearly shows a dramatic shift: the time from founding to first funding has compressed significantly. Back in 2014, companies were waiting nearly 5 years to secure their first round. Fast forward to 2023, and that timeline has dropped to under a year. This isn’t just a reflection of increasing investor confidence in longevity biotech; it’s a signal that the entire funding ecosystem has evolved. Investors are no longer waiting for companies to demonstrate long-term feasibility — they’re placing earlier bets on high-risk, high-reward technologies. Emerging companies are also entering the market with stronger scientific foundations, clearer regulatory pathways, and experienced teams, making them more attractive for early investment. The key takeaway is that the funding process in longevity biotech has become faster and more strategic, signaling a more mature and competitive ecosystem where both risks and opportunities are better understood and managed.

3. Increasing capital and diverse funding strategies

The longevity investment landscape has evolved dramatically since Laura Deming launched The Longevity Fund in 2011 with just $4M. Fast forward to 2022, and the sector has exploded, with more than 20 funds and holding companies focused squarely on longevity, many managing hundreds of millions in capital. Major players like Hevolution, backed by Saudi Arabia, are leading the charge with a staggering $1B per year dedicated specifically to longevity biotech.

Traditional multi-sector giants like ARCH Venture Partners and Khosla Ventures are also getting serious about the space, each backing over five companies. Meanwhile, new funding models are shaking up the scene — crypto-driven initiatives like VitaDAO and IP-NFTs are fundamentally reshaping how capital is raised and distributed across the sector. Notably, VitaDAO, founded in 2021, has already become one of the most active investors in the space, outpacing many traditional funds.

The message is clear: longevity isn’t just a niche anymore, it’s becoming a serious investment theme with increasingly bigger checks and innovative approaches to capital deployment.

Over the past decade, longevity biotech has come a long way. What once seemed like science fiction is now a rapidly evolving field with billions of dollars in investment and a growing ecosystem of startups making strides in therapeutic innovation, with startups like BioAge pushing the industry closer to the mainstream.

However, despite the success of later-stage companies, the pace of new venture formation has slowed, creating a potential bottleneck for future breakthroughs. Critical areas such as genomic instability, ECM stiffness, and certain replacement therapies remain underfunded and underexplored. If innovation stalls here, the sector risks becoming too focused on incremental gains, missing out on bold, paradigm-shifting discoveries.

Enter creative financing strategies. Decentralized platforms like VitaDAO and IP-NFTs are emerging to fill the gap left by traditional venture capital, unlocking new avenues for early-stage companies that might otherwise struggle. Biofoundry is playing a crucial role in this space, bridging the divide between biotech innovation and capital, ensuring that groundbreaking work gets the funding it needs to thrive.

The potential is staggering. Aging drugs could generate $200 billion in revenue, far outpacing the expected $50 billion peak for GLP-1 drugs by 2030. Yet longevity biotech still captures only 2.9% of total biotech funding, highlighting the disconnect between opportunity and current investment. If the ecosystem can fix this imbalance, we’re on the cusp of transforming the way we think about health, aging, and lifespan.